With a market cap of $32.2 billion, NRG Energy, Inc. (NRG) provides retail electricity, energy management, smart home solutions, and carbon management services across the United States and Canada. Through multiple segments, it serves residential, commercial, and industrial customers while operating a diversified portfolio of fossil fuel and renewable energy generation assets and engaging in energy trading and related financial products.

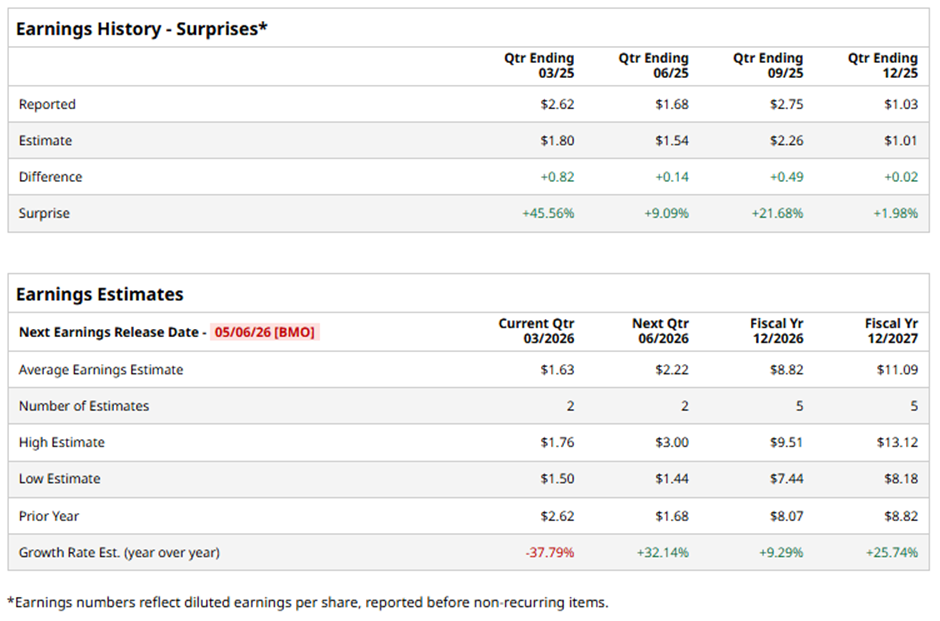

The Houston, Texas-based company is expected to unveil its fiscal Q1 2026 results before the market opens on Wednesday, May 6. Ahead of the event, analysts anticipate NRG to report an adjusted EPS of $1.63, a decrease of 37.8% from $2.62 in the year-ago quarter. However, it has exceeded Wall Street's bottom-line estimates in the past four quarters.

For fiscal 2026, analysts predict NRG Energy to report adjusted EPS of $8.82, a rise of 9.3% from $8.07 in fiscal 2025. Moreover, adjusted EPS is projected to increase 25.7% year-over-year to $11.09 in fiscal 2027.

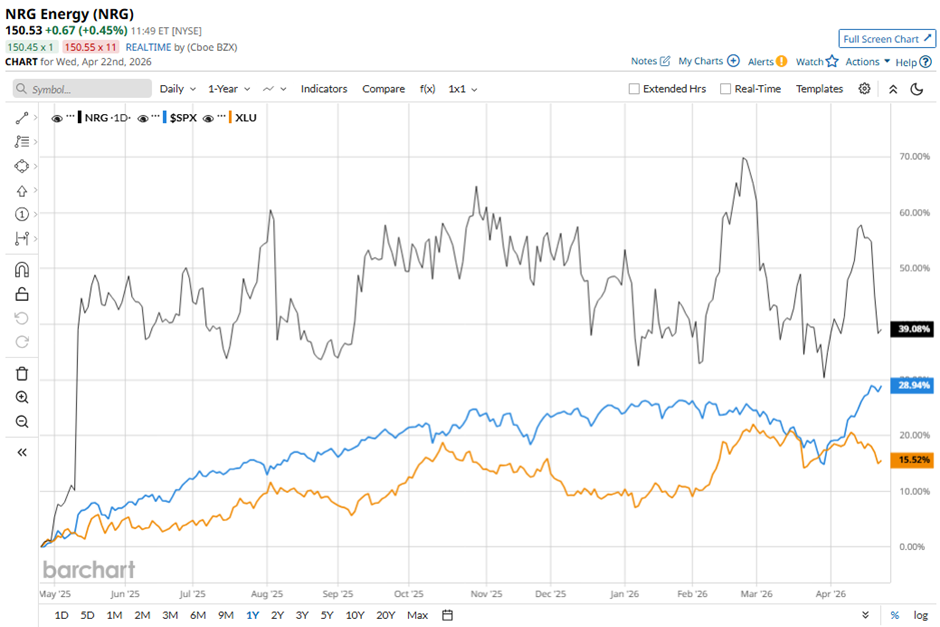

NRG stock has climbed nearly 52% over the past 52 weeks, outpacing the S&P 500 Index's ($SPX) 34.8% gain and the State Street Utilities Select Sector SPDR ETF's (XLU) 15.8% return over the same period.

Shares of NRG Energy rose 4.3% on Feb. 24 after the company reported strong 2025 results, including adjusted net Income of $1.6 billion and adjusted EPS of $8.24, both exceeding prior-year figures. Investor confidence was further boosted by strategic growth moves, particularly the completed acquisition of 13 GW of generation assets and CPower, which doubled its generation capacity and positioned it to benefit from rising power demand.

Additionally, NRG reaffirmed robust 2026 guidance, projecting adjusted EBITDA of $5.3 billion - $5.8 billion and FCF of up to $3.3 billion.

Analysts' consensus rating on NRG stock is bullish, with a "Strong Buy" rating overall. Out of 15 analysts covering the stock, opinions include 12 "Strong Buys" and three "Holds." The average analyst price target for NRG Energy is $211.14, indicating a potential upside of 40.3% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?