Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at First BanCorp (NYSE: FBP) and its peers.

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

The 94 regional banks stocks we track reported a satisfactory Q3. As a group, revenues missed analysts’ consensus estimates by 1.1%.

In light of this news, share prices of the companies have held steady as they are up 4.1% on average since the latest earnings results.

First BanCorp (NYSE: FBP)

Tracing its roots back to 1948 in San Juan, First BanCorp (NYSE: FBP) is a bank holding company that provides commercial banking, consumer financing, mortgage services, and insurance products across Puerto Rico, the U.S. mainland, and the Caribbean.

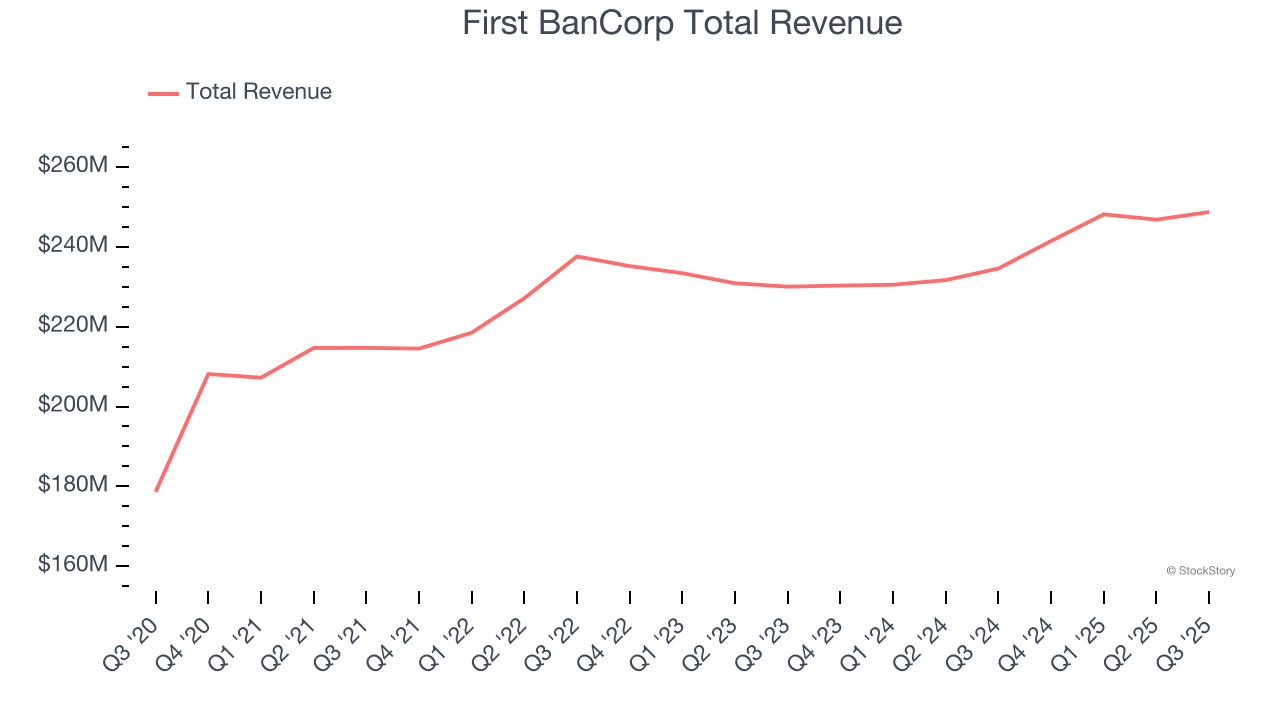

First BanCorp reported revenues of $248.7 million, up 6% year on year. This print fell short of analysts’ expectations by 1.3%. Overall, it was a mixed quarter for the company with a beat of analysts’ EPS estimates but a significant miss of analysts’ net interest income estimates.

Unsurprisingly, the stock is down 2.5% since reporting and currently trades at $20.02.

Is now the time to buy First BanCorp? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Customers Bancorp (NYSE: CUBI)

Originally founded with a "high-tech, high-touch" branch-light banking strategy, Customers Bancorp (NYSE: CUBI) is a bank holding company that provides commercial and consumer banking services through its Customers Bank subsidiary, with a focus on business lending and digital banking.

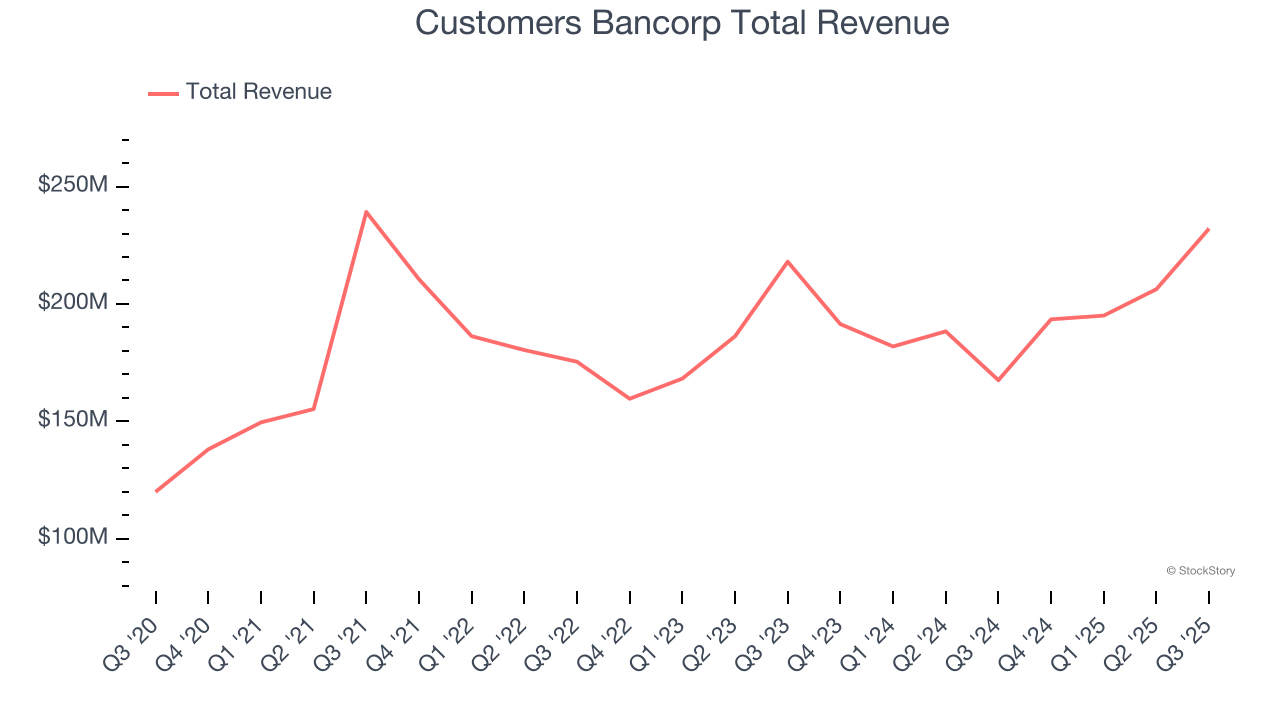

Customers Bancorp reported revenues of $232.1 million, up 38.5% year on year, outperforming analysts’ expectations by 7%. The business had a stunning quarter with a solid beat of analysts’ net interest income estimates and an impressive beat of analysts’ revenue estimates.

The market seems content with the results as the stock is up 4.8% since reporting. It currently trades at $68.72.

Is now the time to buy Customers Bancorp? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: The Bancorp (NASDAQ: TBBK)

Operating behind the scenes of many popular fintech apps and prepaid cards you might use daily, The Bancorp (NASDAQ: TBBK) is a bank holding company that specializes in providing banking services to fintech companies and offering specialty lending products.

The Bancorp reported revenues of $174.6 million, up 38.8% year on year, falling short of analysts’ expectations by 10%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and net interest income estimates.

As expected, the stock is down 16.7% since the results and currently trades at $64.33.

Read our full analysis of The Bancorp’s results here.

FB Financial (NYSE: FBK)

Founded in 1906 and operating through more than a century of economic cycles, FB Financial (NYSE: FBK) operates FirstBank, providing commercial and consumer banking services across Tennessee, Kentucky, Alabama, and North Georgia.

FB Financial reported revenues of $173.9 million, up 94.2% year on year. This number beat analysts’ expectations by 4.2%. It was an exceptional quarter as it also recorded an impressive beat of analysts’ net interest income estimates and a solid beat of analysts’ revenue estimates.

The stock is flat since reporting and currently trades at $56.42.

Read our full, actionable report on FB Financial here, it’s free for active Edge members.

S&T Bancorp (NASDAQ: STBA)

Tracing its roots back to 1902 in western Pennsylvania's industrial heartland, S&T Bancorp (NASDAQ: STBA) is a Pennsylvania-based bank holding company that provides retail and commercial banking services, cash management, trust services, and investment advisory solutions.

S&T Bancorp reported revenues of $103 million, up 6.9% year on year. This result was in line with analysts’ expectations. Aside from that, it was a mixed quarter as its performance in some other areas of the business was disappointing.

The stock is up 13.9% since reporting and currently trades at $40.64.

Read our full, actionable report on S&T Bancorp here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.