Packaging Corporation of America has gotten torched over the last six months - since November 2024, its stock price has dropped 21.6% to $195 per share. This might have investors contemplating their next move.

Is now the time to buy Packaging Corporation of America, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Packaging Corporation of America Will Underperform?

Despite the more favorable entry price, we're cautious about Packaging Corporation of America. Here are three reasons why PKG doesn't excite us and a stock we'd rather own.

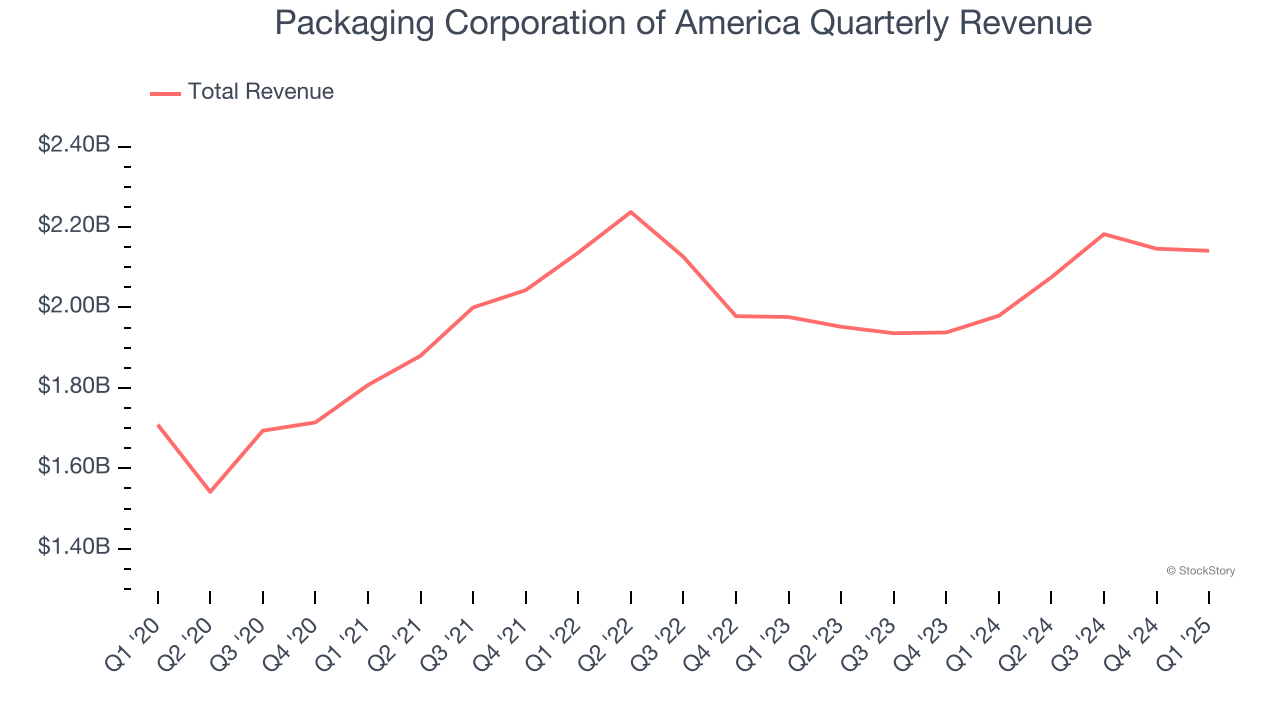

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Packaging Corporation of America grew its sales at a sluggish 4.3% compounded annual growth rate. This fell short of our benchmark for the industrials sector.

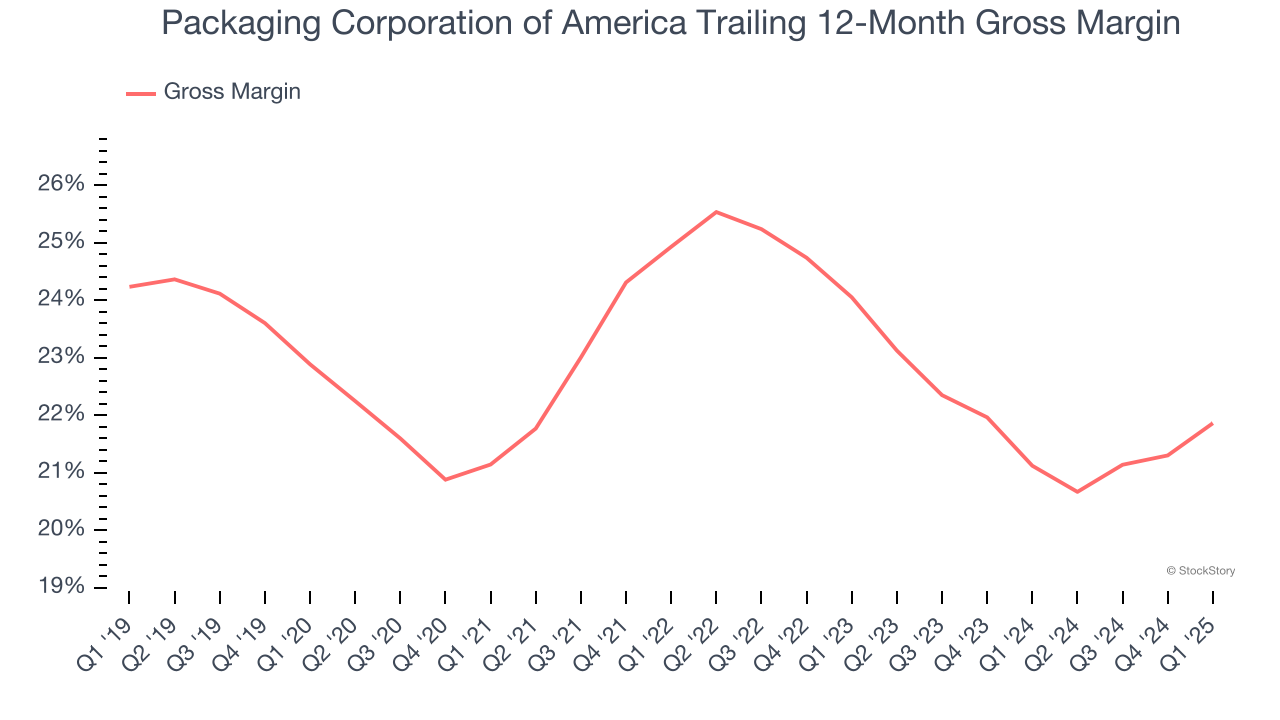

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Packaging Corporation of America has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 22.7% gross margin over the last five years. That means Packaging Corporation of America paid its suppliers a lot of money ($77.32 for every $100 in revenue) to run its business.

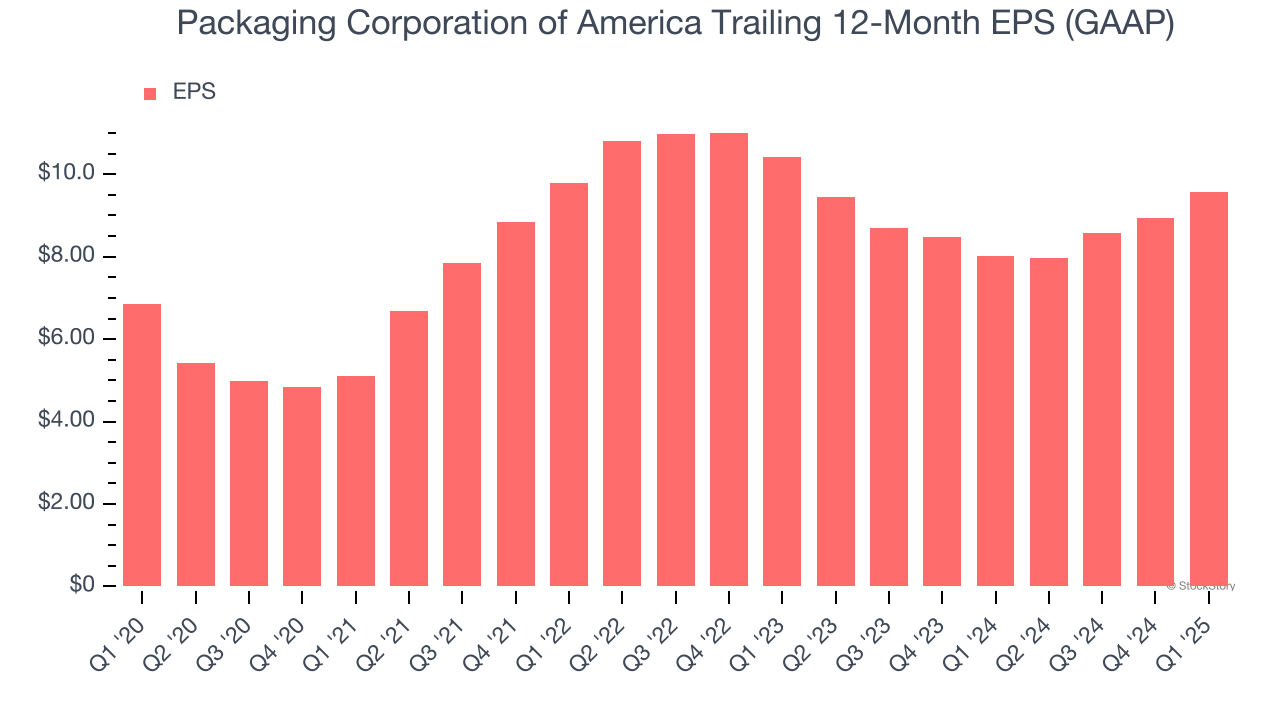

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Packaging Corporation of America’s EPS grew at an unimpressive 6.9% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 4.3% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

We see the value of companies helping their customers, but in the case of Packaging Corporation of America, we’re out. After the recent drawdown, the stock trades at 11.8× forward EV-to-EBITDA (or $195 per share). This valuation tells us a lot of optimism is priced in - you can find better investment opportunities elsewhere. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Like More Than Packaging Corporation of America

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.