AutoZone, Inc. (AZO) has been in the business of keeping cars on the road since 1979. The Memphis, Tennessee-based retailer and distributor of automotive parts and accessories has built its entire operation around covering virtually every mechanical need for cars, SUVs, vans, and light trucks.

With a market cap of nearly $51.1 billion, AutoZone also runs a commercial program that extends credit and delivers parts directly to repair shops, markets diagnostic and shop management software through its ALLDATA brand and pushes its own Duralast product line in a serious way.

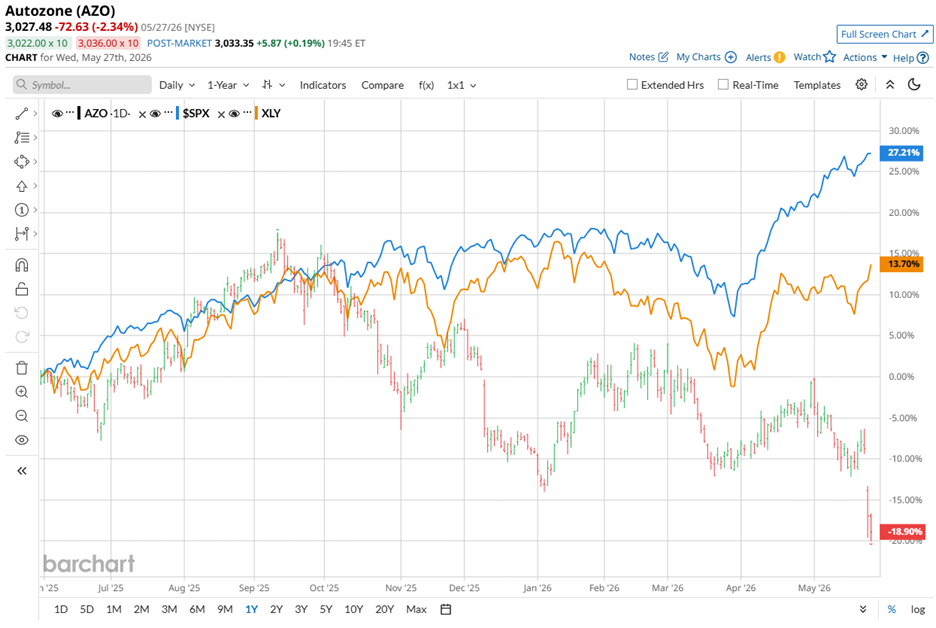

However, the numbers on AutoZone’s price performance over the past year tell a story of persistent underperformance. The stock has fallen 18.1% over the last 52 weeks and is sitting 10.7% in the red year-to-date (YTD).

Meanwhile, the broader market has been in an entirely different league during both periods. The S&P 500 Index ($SPX) climbed 27% over the last 52 weeks and has added 9.9% so far in 2026.

Even at the sector level, AZO stock has struggled to keep pace. The State Street Consumer Discretionary Select Sector SPDR ETF (XLY) has outrun AZO stock as well, gaining 12.1% over the last 52 weeks and rising 1.8% in 2026.

On May 26, AutoZone shares took a nearly 9% hit after the company posted its Q3 2026 results, which fell short of Wall Street expectations and overshadowed a stronger-than-expected profit. Revenue grew 8.4% year over year to $4.84 billion but narrowly missed the analyst forecast of $4.87 billion.

The miss, however, barely moves the needle when weighed against 8.4% growth and solid margin performance. Store count expansion across the U.S., Mexico, and Brazil powered the topline momentum forward, with a 3.9% systemwide comparable sales figure compounding the gains and painting a healthier operational picture than the headline drop suggests.

The margin story landed lighter than feared too, with operating profit climbing approximately 6.5% year over year and EPS of $38.07 running well ahead of the Street’s $36.17 forecast. It seems as if AZO stock is working through a much-needed price correction right now, and for investors willing to play the long game, the correction is quietly building what could shape up to be a generational buying opportunity.

For the full fiscal year 2026, which ends in August, analysts are projecting diluted EPS growth of 3.1% year over year to $149.35. That said, the company has missed its EPS estimates in three of the past four quarters, which adds a note of caution to the outlook.

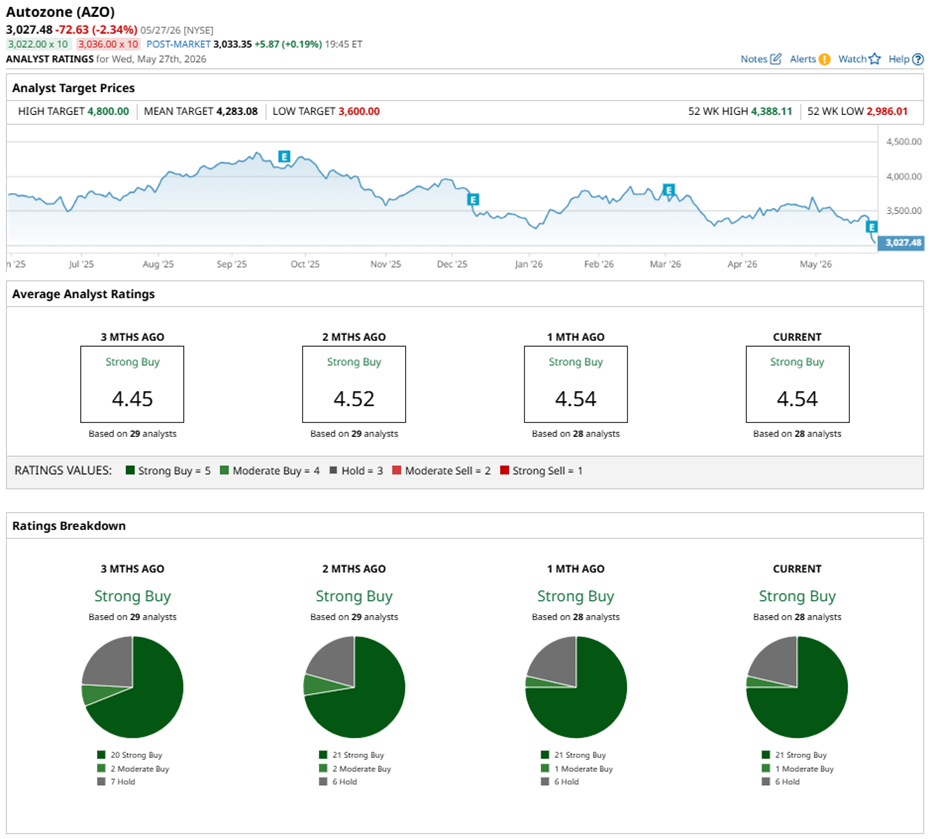

Wall Street is not backing away from AutoZone despite the recent turbulence. Its stock currently holds an overall "Strong Buy" rating. Among 28 analysts covering the stock, 21 carry a "Strong Buy" rating, one recommends a "Moderate Buy," and six advise to "Hold."

The current analyst sentiment also picked up steam compared to three months ago, when 20 analysts held a "Strong Buy" position, meaning confidence has gradually grown even as the share price has pulled back.

On May 27, Kate McShane from Goldman Sachs stepped in and trimmed her price target on AZO stock from $4,345 to $4,096, though Goldman's "Buy" rating on the stock remains in place.

Despite the volatile backdrop, analysts see real and meaningful upside waiting on the other side. The stock's average price target sits at $4,283.08, which implies potential upside of 41.5%. The Street-High target of $4,800 goes even further, representing a jump of 58.5% from current levels.

For investors with the patience to sit through the near-term noise, the targets suggest that the analysts who know this name best believe the best days for AZO stock are still ahead.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Micron Stock Just Added 3X More Value in One Day Than the Entire Company Was Worth Last Year

- Amazon Max Pain Points to a Price of $235 by June 18th

- Stocks Slip Before the Open as U.S.-Iran Flare-Up Lifts Oil and Bond Yields, PCE Inflation Data in Focus

- This High-Yield Defense Stock Just Hiked Its Dividend Nearly 7%