November 19, 2025 – As the global financial markets look ahead to 2026, a significant divergence is emerging in the outlook for the oil and gas sectors. While crude oil markets are poised to grapple with an increasing supply surplus and downward pressure on prices, natural gas is set to experience robust demand growth, primarily driven by burgeoning liquefied natural gas (LNG) exports, leading to strengthening prices. This bifurcated forecast suggests a complex and challenging landscape for energy companies and investors alike, demanding strategic agility in the face of evolving market dynamics.

The coming year, 2026, appears to be a pivotal period where the energy transition, coupled with geopolitical factors and economic shifts, will manifest distinctly across different hydrocarbon segments. The anticipation of substantial crude oil inventory builds could test the resilience of producers, while the escalating global appetite for natural gas, particularly from Asia and Europe, positions it as a critical transition fuel, promising a more favorable environment for gas-focused enterprises.

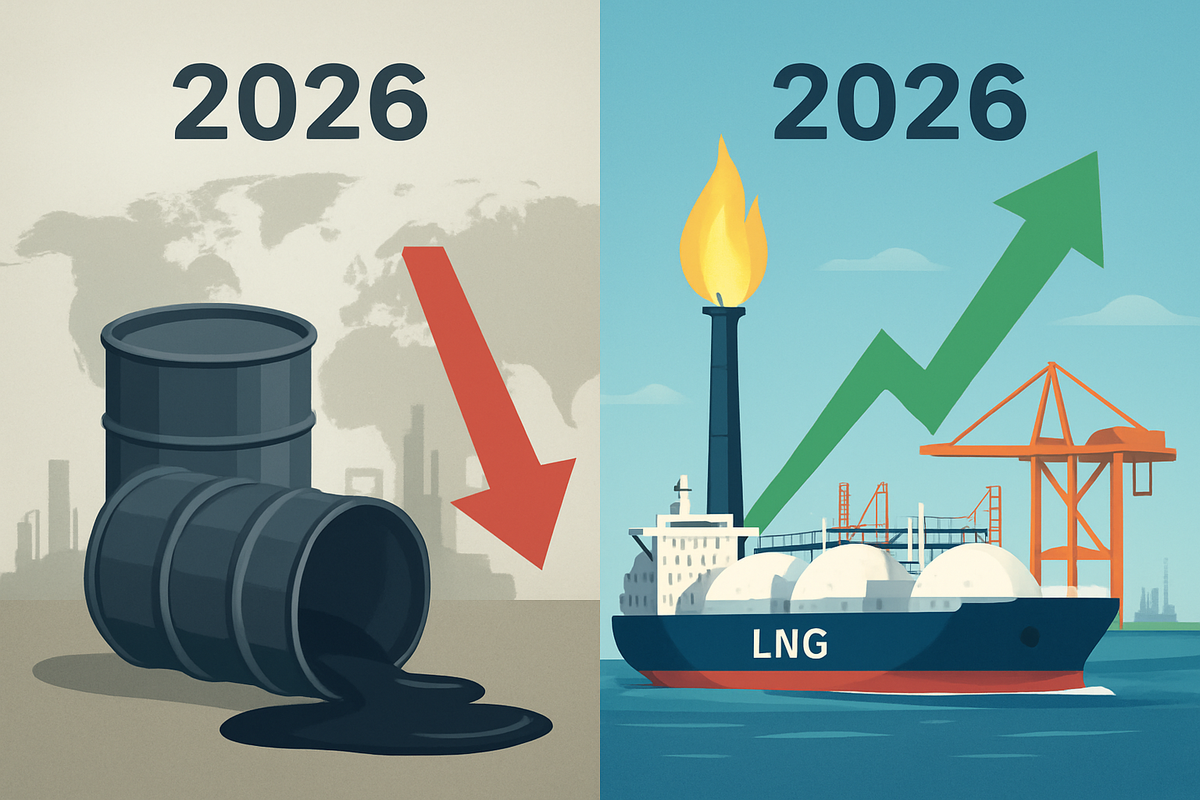

A Tale of Two Hydrocarbons: Production, Consumption, and Price Forecasts for 2026

The detailed outlook for 2026 reveals a stark contrast between crude oil and natural gas. For crude oil, an oversupply scenario is expected to dominate, largely influenced by increasing production from non-OPEC+ nations and the gradual unwinding of production cuts by the OPEC+ alliance. The U.S. Energy Information Administration (EIA) projects global liquid fuels production to increase by 2.8 million barrels per day (b/d) in 2025 and an additional 1.4 million b/d in 2026. Non-OPEC+ countries, including the United States, Brazil, Guyana, and Canada, are slated to be the primary drivers of this growth. Specifically, U.S. crude oil production is forecast to reach an all-time high of approximately 13.6 million b/d in December 2025, although it may see a slight decline to 13.3 million b/d in 2026. OPEC+ is also expected to contribute to the supply increase as they unwind production cuts, with anticipated increases of 0.5 million b/d in both 2025 and 2026. The International Energy Agency (IEA) further projects world oil supply to reach 108.7 million b/d in 2026.

On the demand side, global oil consumption growth is anticipated to be modest, driven almost entirely by non-OECD countries. The EIA forecasts an increase of 1.0 million b/d in 2025 and 1.1 million b/d in 2026. A significant trend is the potential for oil use in transportation to begin declining in 2026, with peak oil demand potentially in sight after 2028 due to the accelerating energy transition and slower economic growth in key regions like China and Europe. This imbalance between rising supply and moderating demand is expected to exert significant downward pressure on crude oil prices. The EIA forecasts Brent crude oil prices to average $55 per barrel (b) in 2026, a substantial drop from an average of $69/b in 2025, with prices potentially falling into the low $50s in early 2026. J.P. Morgan Research has similarly lowered its Brent price forecast to $58/b for 2026, while Goldman Sachs predicts Brent will average $56/b, citing a large market surplus and potential for prices to even dip into the $40s if non-OPEC supply proves more resilient or a global recession materializes. Consequently, global oil inventories are expected to increase significantly through 2026, averaging 2.2 million b/d builds.

In stark contrast, the natural gas market is poised for a robust 2026. While U.S. dry natural gas production is expected to be relatively flat in 2026 compared to 2025, averaging around 116 Bcf/d, global demand is projected to accelerate significantly. This surge in demand is primarily attributed to the continued ramp-up of liquefied natural gas (LNG) exports and growing electricity demand, particularly from energy-intensive sectors like data centers and cryptocurrency mining facilities. The U.S. is expected to export 16 billion cubic feet per day (Bcf/d) of LNG in 2026, representing an additional 10% increase from 2025, making LNG exports the largest incremental call on natural gas demand. Consequently, natural gas prices are forecast to strengthen. The EIA projects the Henry Hub natural gas spot price to average around $4.00 per million British thermal units (MMBtu) in 2026, a notable 16% increase from 2025, driven by demand growing faster than supply amid relatively flat domestic production.

Navigating the Currents: Potential Winners and Losers in 2026

The divergent outlook for crude oil and natural gas in 2026 will undoubtedly create distinct sets of winners and losers across the energy sector. Companies with a significant focus on natural gas production, processing, and particularly LNG exports are likely to emerge as beneficiaries. For instance, major LNG players like Cheniere Energy (NYSE: LNG), with its expansive Sabine Pass and Corpus Christi liquefaction facilities, are well-positioned to capitalize on surging global demand and higher prices. Similarly, natural gas-focused exploration and production (E&P) companies such as EQT Corporation (NYSE: EQT), the largest natural gas producer in the U.S., could see improved profitability and increased investment in their operations. Midstream companies involved in natural gas gathering, processing, and transportation, like Kinder Morgan (NYSE: KMI), which operates extensive natural gas pipeline networks and LNG infrastructure, may also experience increased throughput and revenue.

Conversely, companies heavily weighted towards crude oil production, especially those with higher operating costs or less diversified portfolios, may face headwinds. Oil-focused E&P companies operating in mature basins or those without significant hedging strategies could see their margins squeezed by lower crude prices. While integrated oil majors like ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have diversified portfolios including refining and petrochemicals, their upstream oil segments could face profitability challenges, potentially impacting their overall earnings. However, these majors might mitigate some of the impact through their natural gas and LNG assets, as well as by benefiting from lower crude input costs in their refining operations. Oilfield service companies, such as Schlumberger (NYSE: SLB) or Halliburton (NYSE: HAL), might experience a mixed bag, with reduced drilling activity in some oil basins potentially offset by increased activity in natural gas-rich regions or international markets. Refiners, on the other hand, could see a boost in margins due to cheaper crude feedstock, but this benefit might be tempered by moderating demand for refined products in certain markets.

Broader Implications: Geopolitics, Energy Transition, and Market Shifts

The 2026 oil and gas outlook is not merely about supply and demand figures; it's deeply interwoven with broader industry trends, geopolitical dynamics, and evolving energy policies. Geopolitical risks, such as ongoing conflicts in Ukraine and instability in the Middle East, remain a critical wildcard. While the fundamental outlook points to an oil surplus, any significant supply disruption stemming from these tensions could temporarily inject volatility and upward price pressure, challenging the prevailing bearish sentiment. However, the market's increasing resilience to such shocks, coupled with strategic petroleum reserves, might limit their long-term impact on prices.

The accelerating energy transition continues to be a foundational trend. While it is clearly moderating oil demand growth, particularly in OECD countries, natural gas is increasingly positioned as a crucial "transition fuel." Its lower carbon footprint compared to coal makes it a preferred choice for electricity generation in many regions, thereby underpinning its robust demand growth. This dynamic is influencing policy decisions, with many governments supporting natural gas infrastructure development, especially LNG import and export terminals, to ensure energy security and facilitate the shift away from higher-emitting fossil fuels. Regulatory frameworks are also evolving, with increasing scrutiny on methane emissions from natural gas operations, which could lead to new compliance costs and technological advancements for producers.

Historically, periods of significant oil oversupply have often led to strategic adjustments by major producers, sometimes involving coordinated production cuts to stabilize prices. The current discrepancy between OPEC's "roughly balanced" market view and the IEA's warning of a substantial surplus in 2026 highlights a potential point of contention that could influence future OPEC+ decisions. If inventories build as projected, the pressure on OPEC+ to implement deeper or sustained cuts might intensify, potentially altering the supply trajectory. The parallel growth in renewables, while not directly competing with all aspects of oil and gas, consistently adds downward pressure on overall fossil fuel demand in the long run, forcing companies to diversify their portfolios and invest in cleaner energy solutions.

The Road Ahead: Strategic Pivots and Emerging Opportunities

Looking beyond the immediate forecasts for 2026, the oil and gas industry faces a landscape demanding continuous strategic pivots and adaptation. In the short term, crude oil producers will likely focus on capital discipline, cost optimization, and maximizing efficiency from existing assets to weather the low-price environment. Mergers and acquisitions could become more prevalent as companies seek economies of scale or divest non-core, higher-cost assets. For natural gas players, the emphasis will be on expanding LNG export capacity and securing long-term supply contracts to meet growing global demand. Investment in associated gas capture technologies will also be crucial to monetize gas produced alongside oil, reducing flaring and enhancing environmental performance.

In the long term, the trajectory of the energy transition will dictate the strategic direction of major energy companies. Diversification into renewable energy, carbon capture, utilization, and storage (CCUS), and hydrogen production will become increasingly vital. Companies that can successfully integrate these new energy ventures into their existing operations will be better positioned for sustainable growth. For instance, BP (NYSE: BP) and Shell (NYSE: SHEL) are already making significant investments in offshore wind, solar, and EV charging infrastructure, signaling a broader strategic shift. Market opportunities will emerge in areas like sustainable aviation fuels, blue hydrogen (produced from natural gas with CCUS), and advanced materials for energy storage. Challenges will include navigating evolving regulatory landscapes, securing financing for new energy projects, and managing the decline of legacy fossil fuel assets.

Potential scenarios for the coming years include a prolonged period of lower oil prices if supply continues to outpace demand and OPEC+ struggles to maintain cohesion. Conversely, a sudden geopolitical shock or an unexpected acceleration in global economic growth could tighten the oil market more quickly than anticipated. For natural gas, the primary uncertainty lies in the pace of new LNG project development and the long-term commitment of importing nations to gas as a transition fuel versus a direct leap to renewables. Companies that can demonstrate a clear path to decarbonization while reliably supplying energy will be best positioned for success.

Comprehensive Wrap-up: Navigating a Divided Energy Future

In summary, the 2026 outlook for the oil and gas markets is characterized by a significant divergence: an oversupplied crude oil market facing downward price pressure, and a robust natural gas market driven by strong demand and rising prices. Key takeaways include the relentless growth in non-OPEC+ oil supply, particularly from the U.S., moderating global oil demand, and substantial inventory builds for crude. Conversely, natural gas demand, propelled by LNG exports and electricity generation, is set to outpace supply, leading to higher prices.

Moving forward, the market will require careful navigation. Investors should watch for OPEC+'s responses to the growing oil surplus, the actual pace of global economic growth, and the impact of energy transition policies on both oil and gas demand. For crude oil, monitoring inventory levels and the resilience of U.S. shale production will be crucial. For natural gas, tracking LNG export capacity additions and global demand dynamics, especially from Asia, will be key indicators. Companies with diversified portfolios, strong balance sheets, and a clear strategy for both traditional hydrocarbons and new energy ventures will be better equipped to thrive in this complex and evolving energy landscape. The year 2026 promises to be a test of adaptability and strategic foresight for the entire oil and gas industry.

This content is intended for informational purposes only and is not financial advice